You finally sit down to write your will — something you’ve meant to do for years. You name an executor and outline who should get what. It feels like a responsible milestone, maybe even a relief. Estate, planned. That moment can feel like the finish line. It isn’t, though.

A Will Is Just the Start

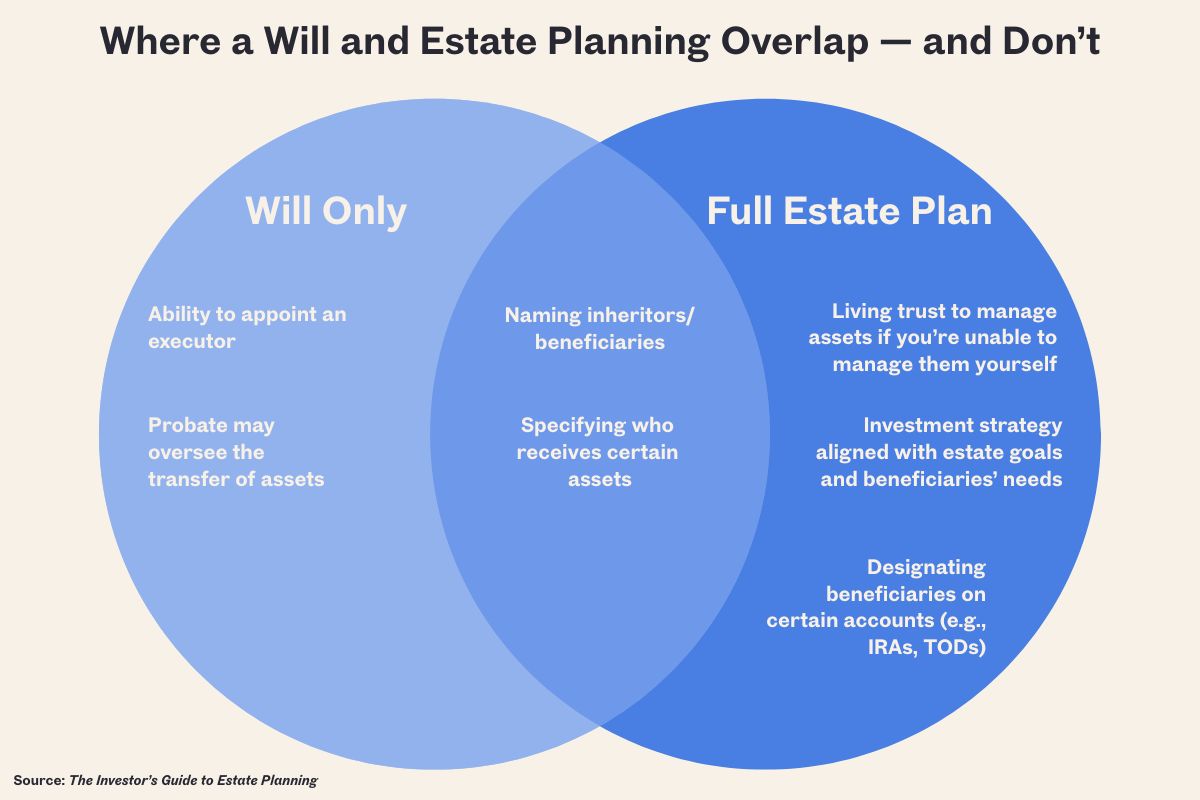

A will is one of the clearest ways to document your wishes. It lets you name someone to manage your estate and spell out who should receive specific assets, but it doesn’t necessarily simplify what comes next. Even with a will in place, your estate may still go through probate, the court process that oversees how assets are distributed.

But without a will or trust at all, state law may determine who receives your estate. So, yes, having a will is important, but it’s just one part of a full plan.

Other Tools for Estate Planning

Certain investment accounts, such as IRAs or transfer-on-death (TOD) accounts, let you name beneficiaries directly. These designations are often set and forgotten, but they play a major role in what actually happens with your assets. You can name both primary and contingent beneficiaries, and unless you update them, those choices typically stay in place.

Living trusts are another option. These written agreements let you name someone to manage your assets and specify who will receive them. Unlike a will, a living trust can also help if you become unable to manage your finances during your lifetime. Someone you trust could step in and handle things on your behalf, without waiting for a court’s permission.

For some investors, beneficiary designations and trusts don’t replace a will; they work alongside it. Each tool serves a different purpose, and understanding where they overlap can help clarify how a complete plan fits together.

It Only Works If the Money Adds Up

Estate planning isn’t just about completing the proper paperwork. Your investment strategy is equally important. If you aim to leave a specific amount behind, your portfolio must support that objective.

If you’re leaving assets to younger family members or organizations, there’s a chance they’ll need to rely on that money for years to come. That calls for a portfolio built for long-term growth. A plan on paper only works if the investment strategy is designed to execute it.

How to Turn Plans Into Peace of Mind

The process is complicated. That’s the simple truth, but doing the work to organize your estate while you’re still living ensures your plan will be properly executed. A will is an important starting point, but it may not cover everything on its own. Beneficiary designations, trusts, and investment decisions all shape what happens down the line.

For some people, that means thinking through how a spouse will access shared assets. For others, it’s about lessening the burden for adult children or fulfilling a charitable goal. Everyone’s reasons are different, but the value of a clear, connected plan is the same.

If you want a better sense of how these tools work together and what to consider next, Fisher Investments’ Investor’s Guide to Estate Planning can help.

Download Fisher Investments’ Investor’s Guide to Estate Planning to start planning your estate.

This story was paid for by an advertiser. Better Report’s editorial staff was not involved in the creation of this content.

This story was paid for by an advertiser. Better Report's editorial staff was not involved in the creation of this content.